Mostly summarized from Gregory Mankiw’s Principles of Economics, 5th Ed.

PART 5 Firm Behavior

and the Organization of Industry

Chapter

14 of 36

Firms

In Competitive Markets

Section

20 of 24

…

Figure

7 here

…

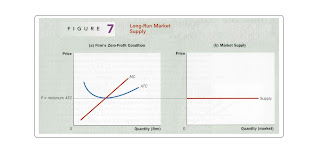

Per Figure

7 panel (a)

In the long run

firms enter or exit the market until economic profit is driven to zero.

If price (P) > average total costs (ATC) there

are profits, this encourages new firms to enter the market.

If P < ATC there are losses, this encourages

some existing firms to exit the market.

…

The process of firms entry into and exit from the

market ends when P settles at ATC.

Each

competitive firm maximizes profits (or minimizes losses) by choosing a quantity

at which P = marginal cost (MC)

Market

free entry and exit eventually forces P = ATC.

Therefore

at market equilibrium, P = MC = ATC and

there is no further market entry and exit.

MC =

ATC only when the firm is operating at minimum ATC.

…

Panel

(a) shows a firm’s long-run equilibrium lowest cost efficient scale.

P = MC, so the firm is profit-maximizing.

P =

ATC, so economic profits are zero.

New

firms have no incentive to enter the market and existing firms have no

incentive to leave the market.

In a competitive market, with free entry

and exit

· there

is only one P consistent with zero profit/loss

· it

is where P is at the minimum of ATC

…

Panel

(b) shows the long-run competitive market supply curve must be horizontal at the

given price.

Any

price above minimum ATC

·

would generate economic profits

·

leading to entry of new firms

This

would result in an increase in the total quantity supplied and profit driven

back down to zero.

…

Any

price below minimum ATC

·

would generate economic losses

·

leading to exit of existing firms

This

would result in a decrease in the total quantity supplied and losses driven

back up to zero.

Eventually,

the number of firms in a competitive market

· adjusts

so P equals the minimum of ATC

· resulting

in enough firms and supply to satisfy all the demand at this price

… …

Comments

Post a Comment