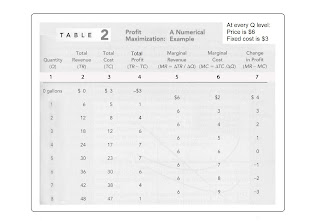

Mostly summarized from Gregory Mankiw’s Principles of Economics, 5th Ed. PART 5 Firm Behavior and the Organization of Industry Chapter 14 of 36 - Firms In Competitive Markets Section 15 of 22 … Figure 5 - Profit as the Area between Price and Average Total Cost The area of the shaded box between price and average total cost (ATC) is the firm's profit, or loss. Height of this box is price (P) minus average total cost, P – ATC (profit per unit). Width of the box is the output quantity, (Q). Panel (a), P is above ATC, the firm has profit. Panel (b), P is below ATC, the firm has loss. … Panel (a) shows a firm with a profit. A firm maximizes profit by producing the Q at which P = MC (MC being average variable costs). The area of the rectangle (P - ATC) x Q is the firm's profit. … Panel (b) shows a firm with a loss . Here the firm wants to minimize losses. This is also achieved by producing the Q where P = MC. The area of the rectangle (ATC - P) x Q is the firm's loss. … A firm ...